Prop Firm Drawdown Rules: The Institutional Guide to Survival (2026)

Master prop firm drawdown rules with institutional-grade strategies. Learn static vs trailing drawdown, position sizing frameworks, and risk management.

TLDR: Prop Firm Drawdown Survival

93% of traders who pass prop firm challenges breach their accounts within 90 days. Not because they can't trade — many show months of profitable results. They breach because they're playing a game whose rules they've fundamentally misunderstood.

The conventional wisdom is seductive in its simplicity. Risk 1-2% per trade. Set your stop losses. Don't revenge trade. Follow these rules, the gurus promise, and you'll keep your funded account. Yet traders who follow these rules religiously still hit their drawdown limits. The advice isn't wrong — it's incomplete.

Here's what seven years of prop firm termination data reveals: the traders who survive don't just manage risk differently. They think about the account itself differently. They've discovered something the failed 93% miss: in prop trading, your account balance is a lie.

Key Takeaways: Institutional Drawdown Management

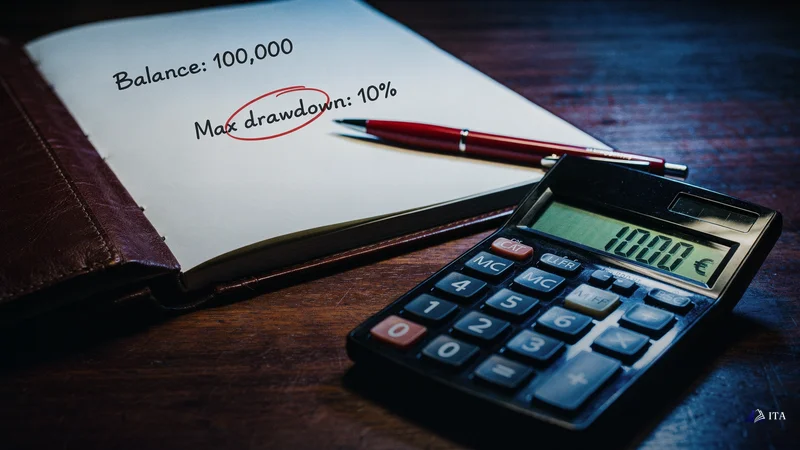

Understanding prop firm drawdown rules and how to survive them starts with a fundamental shift in perspective. Consider this scenario: You have a $100,000 funded account with a 10% maximum drawdown. How much capital do you actually have to trade with?

If you answered $100,000, you're already thinking like the majority who fail. The survivors know the answer is $10,000. That's your real trading buffer. The other $90,000? That's the floor, touch it and you're done.

This isn't just philosophical thinking. It's mathematical precision. When you size positions from $100,000, a few normal losses can breach your limit. When you size from $10,000, those same losses barely dent your buffer. The difference isn't the strategy. It's the denominator. See Prop Trading Firm Rules Explained for more.

Let me show you the framework that changes everything. Traditional position sizing starts with account balance and works forward: "I have $100,000, I'll risk 1%, so $1,000 per trade."

Institutional sizing (the model successful traders use) starts with maximum drawdown and works backward: "I have $10,000 in drawdown buffer, I'll risk 10% of that, so $1,000 per trade."

This approach to prop firm drawdown rules creates an entirely different risk profile. Your position sizes become naturally conservative. Your psychology shifts from protecting profits to preserving capital. Most importantly, you develop the institutional mindset that separates professionals from gamblers.

The Mathematics of Prop Firm Drawdown: Static vs Trailing Models

Same dollar risk. Completely different psychology. When you're sizing from the buffer, every loss is a percentage of your funded account, not an abstraction. You feel the weight of each decision because you're working with the actual constraint.

The static versus trailing distinction becomes critical here. With static drawdown, your $10,000 buffer is fixed. Win or lose, the floor stays at $90,000. But trailing drawdown, the model most instant account firms now use, moves that floor up with your equity highs. Hit $103,000 in floating profit? Your new floor is $93,000. Your buffer hasn't grown; it's shifted.

This is where the 93% get slaughtered. They see profit and increase position size, thinking they have more cushion. But trailing drawdown means your risk capacity never truly expands until the trail locks at your starting balance. Until that lock, every profit is borrowed time.

Daily Loss Limits: The Hidden Account Killer

The daily loss limit adds another layer of complexity. Most firms cap daily losses at 4-5% of the account — seemingly generous. But here's the trap: that's 40-50% of your funded account (the drawdown buffer) in a single day. One bad session can cut your tradeable capital in half.

The institutional approach? Never risk more than 60% of your daily limit. On a $100,000 account with a $5,000 daily limit, stop at $3,000 in losses. Yes, you're leaving risk on the table. That's the point. The buffer isn't just for catastrophic days — it's for normal variance.

Psychology amplifies these mathematical realities. When traders see a $100,000 balance, they anchor to that number. Every $1,000 loss feels like a 1% nick — manageable, recoverable. But when you reframe it as 10% of your funded account, the weight changes. Suddenly, that casual Friday afternoon trade doesn't seem so casual.

Position Sizing from Drawdown: The Institutional Framework

Understanding prop firm drawdown rules and how to survive them starts with position sizing strategy. The data on instant funding accounts reveals critical insights. These programmes advertise "no evaluation" as a benefit, but their drawdown rules are often tighter. They typically enforce 6-8% maximum versus 10-12% for challenge accounts. Most use aggressive trailing mechanisms. These can lock you into a narrow range after just one winning day.

At Institutional Trading Academy, we see this pattern daily. Traders come to us after losing multiple funded accounts, all with the same story. "I was profitable, but I hit the limit." When we analyse their trades, the issue is always the same. They sized positions for a $100,000 account when they had a $10,000 account. See Prop Firm Without Consistency Rules for more.

The firm-specific variations matter, but less than you'd think. Whether it's FTMO's static drawdown calculation or Topstep's end-of-day assessment, the core principle remains: size from the buffer, not the balance. The traders who last aren't necessarily better at predicting markets. They're better at mathematics.

Key Position Sizing Rules for Prop Firm Survival:

- Calculate risk per trade as percentage of drawdown limit, not account balance

- Use maximum 1-2% of available drawdown per position

- Account for correlation between open positions

- Monitor real-time drawdown, especially with trailing rules

This mathematical approach to prop firm drawdown rules separates successful traders from those who repeatedly fail evaluations.

Instant Account Drawdown Mechanics: 2026 Analysis

This extends to multi-account management. Many traders, after getting funded, immediately apply for additional accounts. More accounts, more profit potential, right? Only if you aggregate the drawdown limits. Three $100,000 accounts with 10% drawdown aren't three separate $100,000 pools — they're one $30,000 pool spread across three risk buckets.

The psychological framework for survival isn't about motivation or discipline in the traditional sense. It's about cognitive reframing. Every funded account is a drawdown management exercise disguised as a trading opportunity. The profit targets are secondary. The drawdown is primary. See Prop Trading Firm Rules Explained for more.

Here's the checklist the 7% use before every trade:

- Current drawdown buffer (not account balance)

- Percentage of buffer at risk (not percentage of account)

- Daily loss accumulated (as percentage of daily limit)

- Trailing drawdown position (if applicable)

- Aggregated risk across all positions

Psychological Frameworks for Drawdown Survival

Notice what's missing? Win rate. Profit targets. Technical analysis. Those matter for profitability. But for prop firm survival, they're secondary to position sizing mathematics.

The 2026 regulatory landscape has actually tightened these constraints. New oversight has pushed firms toward stricter enforcement and real-time monitoring. The days of "soft breaches" and second chances are largely over. When you hit the limit, the algorithm doesn't care about your story.

So what should you do differently starting today? First, recalculate every position size using the buffer as your base. On a $100,000 account with 10% drawdown, your position sizes should reflect a $10,000 account. Second, implement the 60% daily stop rule. Third, if you trade instant account accounts, assume zero buffer growth until trailing locks.

Firm-Specific Drawdown Analysis: 2026 Landscape

The uncomfortable truth is this: prop firm trading isn't about making money. It's about not losing money while making money. The traders who survive understand this paradox. They've stopped trying to maximize returns and started trying to minimize the probability of ruin.

Your funded account balance is a mirage. Your drawdown buffer is your funded account. Size accordingly, and you might just join the 7% who make it past 90 days. Size from the balance, and you're already writing your termination story.

The math is unforgiving. But then again, so is the market.

Frequently Asked Questions

What is the difference between static and trailing drawdown in prop firm trading?

Static drawdown keeps a fixed floor regardless of profits — on a $100,000 account with 10% static drawdown, the floor stays at $90,000 forever. Trailing drawdown moves the floor up with your equity highs in real-time, meaning your risk buffer shifts but doesn't grow until the trail locks at your starting balance.

Why do traders fail prop firm challenges even when they are net profitable?

93% of traders breach their accounts within 90 days because they size positions from the account balance instead of the drawdown buffer. A $100,000 account with 10% drawdown has only $10,000 in funded account — sizing from $100,000 makes normal losses breach the limit even with profitable trading.

How should I size my positions to stay within prop firm drawdown rules?

Size positions from your drawdown buffer, not the account balance. On a $100,000 account with 10% drawdown, treat it as a $10,000 account for position sizing. Never risk more than 60% of your daily loss limit in a single session to preserve your buffer for normal variance.

Are instant account prop firms harder to survive because of drawdown rules?

Yes, instant account programmes typically use tighter maximum drawdowns of 6-8% versus 10-12% for challenge accounts, plus aggressive trailing mechanisms that can lock you into narrow ranges after one winning day. The 'no evaluation' benefit comes with stricter ongoing risk constraints that make survival more difficult.

How is drawdown calculated in prop firm accounts?

Most prop firms calculate drawdown from real-time equity including open trades, meaning floating losses count toward both daily and maximum drawdown breaches immediately. This makes position sizing and timing critical, you can breach limits even before closing losing positions if they move too far against you.

Key Takeaways

- Size positions from your drawdown buffer ($10,000), not your account balance ($100,000) — this single shift prevents 93% of breaches.

- Never risk more than 60% of your daily loss limit in one session to maintain buffer for normal market variance.

- Trailing drawdown means profits are borrowed time — your risk capacity never expands until the trail locks at starting balance.

- Aggregate drawdown limits across multiple accounts — three $100K accounts equal one $30K risk pool, not three separate buckets.

- Implement the 5-point pre-trade checklist: current buffer, buffer percentage at risk, daily loss accumulated, trailing position, aggregated exposure.

- Reframe funded accounts as drawdown management exercises disguised as trading opportunities — the limit is primary, profit targets secondary.

- Apply institutional sizing methodology: work backward from maximum drawdown ($10K buffer) rather than forward from account balance ($100K).

Start Your Trading Evaluation

Simulated funded accounts up to $800K. Up to 95% profit split. Backed by a regulated broker.

Get Funded